Australia’s Current Sustainability Reporting Requirements

While Australia has no dedicated sustainable business legislation in place akin to the European Union’s Corporate Sustainability Reporting Directive (2023) and the United Kingdom’s Sustainability Disclosure Standards, there are several existing sustainability reporting requirements which govern business operations.

Australia’s existing sustainability requirements are primarily aimed at encouraging transparency and accountability in relation to environmental, social, and governance (ESG) aspects. Below we outline the current key sustainability reporting frameworks and regulations in Australia, as at FY 2022-2023:

Corporations Act 2001

The Corporations Act requires certain companies, such as large proprietary companies and companies listed on the Australian Securities Exchange (ASX), to disclose information about their operating and financial performance, including any material risks arising from environmental and social impacts.

Australian Securities Exchange (ASX) Corporate Governance Principles and Recommendations

ASX-listed companies are expected to comply with the Corporate Governance Principles and Recommendations, which include reporting on environmental and social risks, strategies, and performance indicators.

The ASX’s released its 4th Edition updates in 2019 which calls out the need for Boards to monitor the adequacy of the entity’s risk management framework and satisfy itself that the entity is operating with due regard to the risk appetite set by the board. This includes satisfying itself that the risk management framework deals adequately with contemporary and emerging risks such as conduct risk, digital disruption, cyber-security, privacy and data breaches, sustainability and climate change.

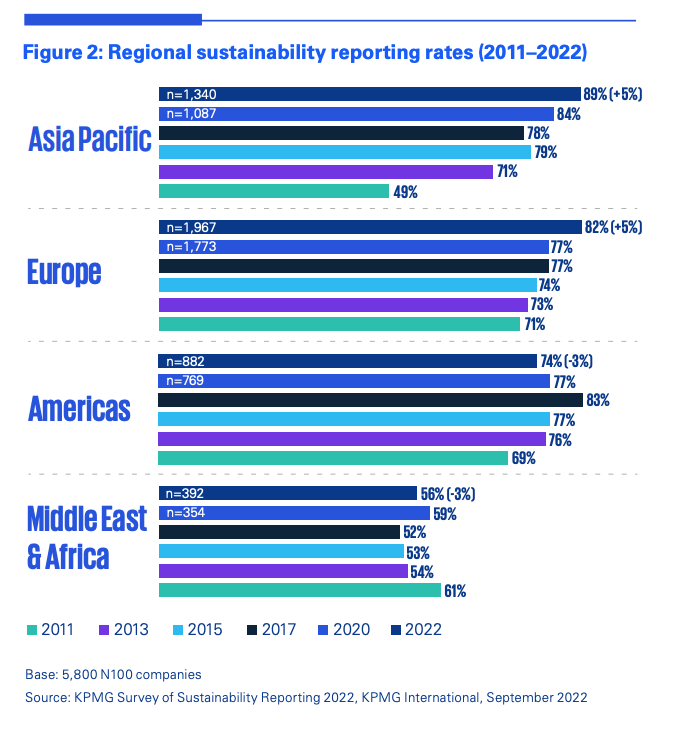

KPMG’s 2022 study of sustainability and ESG reports from 5,800 companies across 58 countries, found that 90 percent of the ASX100 recognise climate as a financial risk, compared to only 64 percent of the largest global 250 companies (the G250)*. This has risen from 78 percent of the ASX100 in the equivalent survey in 2020.

Modern Slavery Act 2018

The Modern Slavery Act 2018 requires businesses with an annual consolidated revenue of over AUD 100 million to report on the risks of modern slavery in their operations and supply chains. This reporting aims to address issues related to forced labor, human trafficking, and slavery-like practices.

Under the Act, the Australian Government is required to maintain an online publicly accessible register of modern slavery statements submitted by reporting entities via the Online Register for Modern Slavery Statements.

The Register was launched on 30 July 2020, and the first tranche of modern slavery statements published on 27 November 2020.

For the first full reporting cycle under the Act, which ended on 30 June 2021, there were close to 2,500 statements submitted to the Register, representing close to 4,500 entities. Complying Modern Slavery Statements can be lodged voluntarily by businesses and organisations as a demonstration of your commitment to the Act’s principals.

NOTE: On 25 May 2023, the Federal government tabled its first review of the Australia's Modern Slavery Act, which reviewed the first 3 years of the Act's operation. Led by Professor John McMillan, AO, supported by the Attorney General’s Department. The review made 30 recommendations for the Government to strengthen the Act. Key recommendations include:

introducing penalties for non-compliance with statutory reporting requirements

lowering the reporting threshold from $100 million to $50 million

requiring entities to report on modern slavery incidents or risks

amending the Act to require entities have a due diligence system in place

strengthening the administration of the Act through proposed legislative amendments and expanded administrative guidance

proposing functions for the federal Anti-Slavery Commissioner in relation to the Act

National Greenhouse and Energy Reporting (NGER) Scheme

The National Greenhouse and Energy Reporting Act 2007 (NGER Act) introduced a single national framework for reporting and disseminating company information about greenhouse gas emissions, energy production and energy consumption. The NGER Scheme applies to energy producing facilities and company groups that meet specific thresholds in terms of emissions or energy consumption.

Facility Thresholds include:

25 kt or more of greenhouse gases (CO2-e) (scope 1 and scope 2 emissions)

production of 100 TJ or more of energy, or

consumption of 100 TJ or more of energy

hresholds for company groups start at

Corporate Group Thresholds include:

50 kt or more of greenhouse gases (CO2-e) (scope 1 and scope 2 emissions)

production of 200 TJ or more of energy, or

consumption of 200 TJ or more of energy

Financial Sector Disclosures

Financial institutions operating in Australia including banks, insurance companies and superannuation funds, are subject to disclosure requirements related to climate-related risks and opportunities. These requirements are issued by regulatory bodies such as the Australian Prudential Regulation Authority (APRA) and the Australian Securities and Investments Commission (ASIC).

APRA takes a broader view on sustainability. Its prudential standard SPS 515 Strategic Planning and Member Outcomes requires trustees to assess whether they will continue to deliver quality, value-for-money member outcomes into the future, and references the impacts of social change and climate risks on its ability to deliver future returns for members.

What’s Ahead for Australia’s Sustainability Regulations and Reporting?

Under the Albanese-led Labor government, with key input from the Greens and independent ‘Teal’ Ministers, Australia’s sustainability regulations and reporting requirements are evolving.

The Australian Government is actively reviewing a range of international sustainability standards, specifically: standards outlined by the Taskforce on Climate-related Financial Disclosures (TCFD) and the Global Reporting Initiative (GRI). At first glance, the Government’s call for consultation papers from industry, educational and science institutions on the application of TFCD based regulations signals the likelihood of future Australian regulations leaning towards this standard. However the EU recently encouraged the Australian Government to review the GRI standards which go beyond the TCFD’s focus on environmental reporting.

Taskforce for Climate-related Financial Disclosures

In recognition of the critical role that capital allocation makes to transitioning the world to more sustainable operations, the Financial Stability Board (FSB) created the Taskforce to develop a framework of the types of information that companies should disclose to report better quality information and support informed capital allocation.

In 2017, the TCFD released its first climate-related financial disclosure recommendations to help companies support investors, lenders, and insurance underwriters in appropriately assess and price risks related to climate change.

Updated in 2021 to include Implementation Guidance, the disclosure recommendations are structured around four thematic areas:

governance

strategy

risk management, and

metrics and targets

Global Reporting Initiative (GRI)

The GRI is the world’s most widely used framework for reporting sustainability - covering economic, environmental and social impacts. The GRI provides a modular framework - including Universal Standards that can apply to any organisation, Sectoral standards that support increased transparency purpose built for industry sectors and Topic Based Standards that cover a broader range of thematics.

The GRI Standards form the basis of the EU’s Corporate Sustainability Directive and were recently updated in June 2023 with enhanced practical guidance for implementation.

While not mandatory in Australia, the GRI framework is widely used by Australian businesses to voluntarily report on their sustainability performance. With its sector specific guidance and indices, many companies choose to align their reporting with GRI guidelines to enhance transparency and comparability.

Australia’s National Climate Risk Assessment

In parallel to reviewing which global sustainability disclosure standards to adopt and or tailor, the Federal Government is undertaking a science-based review of climate risks.

The National Climate Risk Assessment is a two-part evalaution of the risks Australians face due to climate change which commenced in July 2023 and is scheduled to be completed by late 2024. The NCRA seeks to help individuals and industry understand the risks and impacts to Australia from climate change through a range of scenario based modelling and is expected to inform sustainability regulations and reporting requirements.

Shareholder and Consumer Expectations

Even without Government legislations, shareholders, communities and consumers increasingly expect organisations to take the lead on sustainability initiatives. Proactive, voluntary reporting frameworks by organisations are viewed positively as a way to demonstrate their commitment to sustainability, reduce climate and social risk, and create new value.

Are you considering setting sustainability targets for your organisation? Learn how to get started on your sustainability journey.